How to sue my car insurance company with a lawyer’s help? It’s a question many find themselves asking after a frustrating claims process. Navigating the complexities of insurance law can feel overwhelming, but understanding your rights and having legal support is crucial. This guide breaks down the steps involved, from understanding your policy to building a strong case and pursuing legal action.

We’ll cover everything from identifying valid grounds for a lawsuit – like bad faith denial of a legitimate claim – to choosing the right lawyer and understanding the legal process, including mediation, arbitration, and litigation. We’ll also provide practical advice on record-keeping, effective communication with your attorney, and the potential outcomes of your case, including settlements, judgments, and appeals.

Get ready to empower yourself with the knowledge you need to protect your rights.

Understanding Your Insurance Policy

Navigating the complexities of your car insurance policy is crucial, especially when considering legal action. Understanding your policy’s terms and conditions, including claims procedures and legal recourse options, empowers you to effectively pursue your rights. This section will clarify key aspects of a typical policy, helping you prepare for potential disputes.

A standard car insurance policy Artikels the agreement between you and your insurer. It details the coverage provided, your responsibilities, and the process for filing claims. Crucially, it specifies the limits of liability and any exclusions that might affect your ability to recover damages. Understanding these aspects is paramount in determining your options should a claim arise.

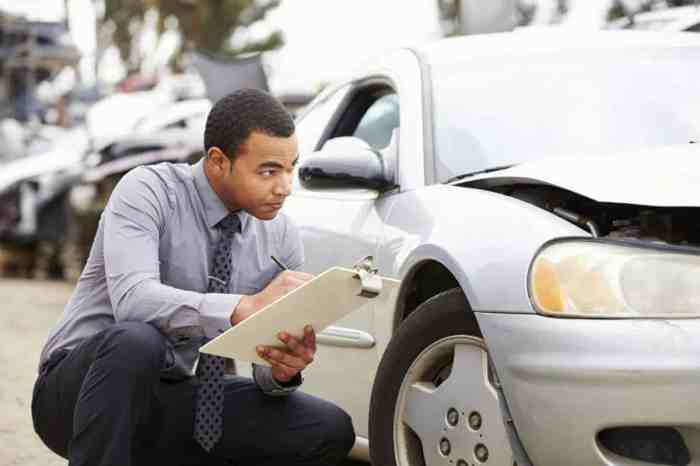

Filing a Claim

The claim filing process typically involves reporting the incident to your insurer within a specified timeframe – often within 24 to 48 hours. You’ll need to provide detailed information about the accident, including the date, time, location, and involved parties. Supporting documentation, such as a police report, photos of the damage, and witness statements, significantly strengthens your claim.

Failure to promptly report the incident or provide necessary documentation can jeopardize your claim. The insurer will then investigate the claim, potentially requesting additional information or conducting an independent assessment of the damages.

Suing your car insurance company can be tricky, but having a skilled lawyer significantly improves your chances of a favorable outcome. The key is finding the right legal representation, which is why knowing how to effectively choose a lawyer is crucial. Check out this helpful guide on How to find the best car insurance lawyer after an accident to navigate this process.

With the right lawyer on your side, you’ll be better equipped to successfully sue your insurance company and get the compensation you deserve.

Policy Coverage Limits and Exclusions

Your policy’s coverage limits define the maximum amount your insurer will pay for covered losses. For example, a liability limit of $100,000 means the insurer will pay a maximum of $100,000 for injuries or property damage caused by you to others. Understanding these limits is crucial, as exceeding them leaves you personally liable for the remaining costs. Exclusions are specific events or circumstances not covered by your policy.

Common exclusions might include damage caused by driving under the influence of alcohol or drugs, or damage resulting from intentional acts. Carefully reviewing your policy to understand these limits and exclusions is essential before engaging in any legal action. For instance, a policy might exclude coverage for damage caused by wear and tear, while another might exclude coverage for accidents occurring outside a specified geographical area.

It’s vital to understand what your policy does and doesn’t cover.

Interpreting Your Policy

Insurance policies often contain complex legal jargon. It’s advisable to carefully read your policy and seek clarification from your insurer if anything is unclear. Look for specific sections detailing your rights and responsibilities in case of an accident or claim. These sections often Artikel the process for dispute resolution, including options for arbitration or litigation. Pay close attention to the definitions of key terms, such as “accident,” “damage,” and “liability,” as these definitions will guide the insurer’s assessment of your claim.

If you find your policy difficult to understand, seeking assistance from an independent insurance professional can be beneficial.

Grounds for Legal Action

Suing your car insurance company is a serious undertaking, often requiring the assistance of a legal professional. Understanding the grounds for such action is crucial before proceeding. This section will Artikel common reasons why individuals find themselves in legal battles with their insurers, emphasizing the importance of understanding your policy and consulting with an attorney.

Reasons for Lawsuit Against Car Insurance Companies

Disputes between individuals and their car insurance companies frequently arise. These disputes can stem from a variety of issues, often leading to legal action. The following table illustrates some common reasons, scenarios, relevant policy clauses, and potential legal outcomes. It is vital to remember that the specifics of each case will heavily influence the outcome.

| Reason for Lawsuit | Example Scenario | Relevant Policy Clauses | Potential Legal Outcomes |

|---|---|---|---|

| Unfair Claim Denial | A driver is involved in a minor accident, clearly the other driver’s fault. The insurance company denies the claim, citing insufficient evidence, despite the driver having a police report and witness testimony. | Claims process section, evidence requirements, policy limits. | The court may order the insurance company to pay the claim, plus potential penalties for bad faith. |

| Unreasonable Claim Settlement Offer | An individual sustains significant injuries and property damage in an accident. The insurance company offers a settlement far below the actual medical expenses and vehicle repair costs. | Settlement procedures, duty to act in good faith, policy limits. | The court may award a larger settlement, potentially including punitive damages if bad faith is proven. |

| Breach of Contract | The insurance company fails to fulfill its contractual obligations Artikeld in the policy, such as failing to provide timely payment for repairs or medical expenses. | Policy terms and conditions, payment deadlines, coverage details. | The court may order the insurance company to fulfill its contractual obligations, plus potential damages for breach of contract. |

| Underpayment of Claim | An individual’s car is totaled in an accident. The insurance company’s valuation of the vehicle is significantly lower than its market value, resulting in an underpayment of the claim. | Valuation methods, total loss settlement procedures, policy limits. | The court may order the insurance company to pay the difference between the offered settlement and the vehicle’s actual market value. |

Bad Faith in Insurance Claims

“Bad faith” in the insurance context refers to an insurer’s unreasonable and unfair conduct in handling a claim. This often involves a conscious disregard for the insured’s rights and the terms of the insurance policy. Examples of actions that could constitute bad faith include: delaying claim processing without justification, denying a claim without proper investigation, failing to communicate effectively with the insured, and offering unreasonably low settlement amounts.

For instance, an insurer might repeatedly request unnecessary documentation or delay payment of legitimate medical bills, causing undue hardship to the insured. Such actions can lead to significant legal consequences for the insurance company.

Denial of Legitimate Claims

Insurance companies may deny legitimate claims for various reasons, some valid and some not. A common scenario involves insufficient evidence, where the insurer claims the claimant hasn’t provided enough proof to support their claim. However, this might be a tactic used to avoid paying a legitimate claim. Another reason might be the insurer incorrectly interpreting the policy’s terms and conditions.

If an insurance company denies a legitimate claim without proper justification, it could be deemed a breach of contract, leading to legal action. The legal implications of such denials can range from court-ordered payment of the claim to substantial penalties for bad faith practices, depending on the specifics of the case and the jurisdiction.

Seeking Legal Counsel

Navigating the complexities of an insurance claim dispute can be daunting, but seeking legal counsel is often crucial for a successful outcome. The right lawyer can significantly improve your chances of receiving a fair settlement. Choosing wisely is key to a positive experience.Choosing the Right Insurance Dispute LawyerSelecting a lawyer specializing in insurance disputes requires careful consideration. You need someone experienced, successful, and well-regarded by their clients.

Don’t just settle for the first name you find.

Lawyer Selection Criteria

Finding a qualified lawyer involves assessing several key factors. Experience in handling similar cases demonstrates their familiarity with the legal landscape and potential strategies. A demonstrably high success rate indicates their effectiveness in achieving favorable outcomes for their clients. Finally, positive client reviews offer valuable insights into their professionalism, communication skills, and overall client experience. These combined factors provide a comprehensive picture of a lawyer’s capabilities.

Questions to Ask Potential Lawyers

Before committing to a lawyer, it’s essential to have a clear understanding of their approach and fees. A well-prepared list of questions will ensure you gather the necessary information to make an informed decision.

- Their experience handling cases similar to yours, including the specific types of insurance policies involved.

- Their success rate in resolving cases like yours, including specific examples of settlements or judgments obtained.

- Their fee structure, including hourly rates, contingency fees (if applicable), and any other potential costs.

- Their communication style and how frequently they will update you on the progress of your case.

- Their strategy for handling your specific case, including potential timelines and challenges.

- References from previous clients who have handled similar cases.

The Attorney-Client Relationship and Costs

The attorney-client relationship is built on trust and open communication. Your lawyer will act as your advocate, guiding you through the legal process and representing your interests in negotiations or court. They will advise you on the best course of action, explain complex legal concepts in plain language, and keep you informed throughout the process.

Typical Attorney Fees

Lawyers typically charge fees based on different models. Hourly rates are common, where you pay for the lawyer’s time spent on your case. Contingency fees are another option, where the lawyer’s fee is a percentage of the settlement or judgment awarded. This is often used in personal injury cases, but its applicability to insurance disputes will depend on the specifics of your case and your lawyer’s agreement.

It’s crucial to understand all fees upfront to avoid unexpected expenses. For example, a lawyer might charge $300 per hour, or a 30% contingency fee on any settlement amount exceeding $10,000. Remember to always clarify all costs, including court filing fees, expert witness fees, and other potential expenses, to ensure financial transparency.

The Legal Process

Suing your car insurance company is a complex undertaking, best navigated with the guidance of legal counsel. Understanding the legal process, however, can empower you to participate more effectively in your case and make informed decisions. The path to resolution often involves several key stages, each with its own set of requirements and potential outcomes.The process typically begins with the filing of a formal complaint outlining the reasons for the lawsuit and the desired outcome.

This complaint, drafted by your lawyer, is submitted to the appropriate court, initiating the legal proceedings. Subsequent stages might involve discovery, where both sides exchange information and evidence, and potentially pre-trial motions to resolve certain issues before a full trial. Depending on the complexity and specifics of the case, the process can range from a few months to several years.

Filing a Complaint and Discovery, How to sue my car insurance company with a lawyer’s help

The initial step involves drafting and filing a formal complaint with the court. This document meticulously details the insurance company’s alleged breach of contract or bad faith practices, providing specific examples and supporting evidence. Following the complaint’s filing, the discovery phase commences. This crucial stage involves both parties exchanging relevant information, including documents, witness statements, and expert opinions. Examples of relevant documents include the insurance policy itself, police reports from the accident, medical bills and records, repair estimates, and correspondence between the insured and the insurance company.

The discovery process aims to ensure transparency and a fair evaluation of the case. Failure to adequately participate in discovery can have serious consequences.

Evidence in Insurance Lawsuits

A successful lawsuit relies heavily on compelling evidence. This evidence can be categorized into several types. Police reports provide objective accounts of accidents, including details on fault and damages. Medical records document injuries sustained, treatment received, and ongoing healthcare needs. Witness statements, if available, can corroborate the insured’s version of events and the extent of damages.

Photographs and videos of the accident scene and damaged property serve as visual evidence. Expert witness testimony, from accident reconstruction specialists or medical professionals, can be invaluable in clarifying complex aspects of the case. Financial records, including repair bills, lost wages, and medical expenses, demonstrate the financial impact of the accident. Each piece of evidence must be carefully authenticated and presented to the court to be considered admissible.

Mediation, Arbitration, and Litigation

Disputes with insurance companies can be resolved through various methods. Mediation involves a neutral third party facilitating communication and negotiation between the insured and the insurance company, aiming to reach a mutually agreeable settlement. Arbitration, similar to mediation, involves a neutral third party, but the decision rendered by the arbitrator is typically binding. Litigation, the most formal and adversarial approach, involves a trial before a judge or jury, where the court determines the outcome based on presented evidence and legal arguments.

Mediation and arbitration are generally less expensive and time-consuming than litigation, offering potentially quicker resolutions. However, litigation provides a more formal avenue to seek a favorable judgment, particularly if settlement negotiations fail. The choice of dispute resolution method often depends on the specifics of the case, the preferences of the parties involved, and the terms of the insurance policy.

Building Your Case

Suing your insurance company is a serious undertaking, requiring meticulous preparation and a strong case. Winning hinges on effectively presenting your evidence and demonstrating a clear violation of your policy. This means more than just recounting your experience; it requires building a comprehensive and irrefutable case.The foundation of a successful lawsuit lies in meticulous record-keeping. From the initial accident report to every communication with your insurance company, maintain a detailed log of all interactions and documents.

This diligence not only strengthens your case but also demonstrates your commitment to resolving the issue fairly. Failing to document these crucial details can significantly weaken your position.

Maintaining Detailed Records

A comprehensive record-keeping system is crucial. This involves gathering all relevant documents related to your claim. This includes, but is not limited to, police reports, medical records, repair estimates, photographs of damages, correspondence with the insurance company (emails, letters, and notes from phone calls), and any other relevant documentation. Consider using a dedicated folder or digital system to organize these materials chronologically.

This allows for easy access and review, both by you and your legal team. The more organized your records, the smoother the legal process will be. For example, if you have multiple medical bills, organize them by date of service and clearly label each document with a sequential number.

Illustrative Timeline of Events

Imagine a scenario where a driver’s car is rear-ended, resulting in significant damage and personal injuries. The following timeline illustrates the events leading up to the decision to sue:

| Date | Event |

|---|---|

| October 26, 2023 | Car accident occurs. Police report filed. |

| October 27, 2023 | Initial claim filed with insurance company. |

| November 15, 2023 | Insurance adjuster contacts the driver. |

| December 10, 2023 | Insurance company offers a settlement deemed insufficient by the driver. |

| January 15, 2024 | Driver’s attorney sends a demand letter to the insurance company. |

| February 28, 2024 | Insurance company refuses to increase settlement offer. |

| March 15, 2024 | Lawsuit filed. |

This timeline demonstrates the progression of events, highlighting the attempts at settlement before resorting to litigation. Each step is documented, providing a clear and concise record of the dispute.

Effective Communication with Your Lawyer

Open and consistent communication with your lawyer is paramount. Regularly update your lawyer on any new developments in your case, including new evidence, communication from the insurance company, or changes in your medical condition. Provide your lawyer with copies of all documents related to your case. Proactive communication prevents misunderstandings and ensures your lawyer is fully informed to build the strongest possible case.

For example, if you receive a new medical bill, forward it to your lawyer immediately. If you have a phone call with the insurance adjuster, take detailed notes and share them with your lawyer. Clear and timely communication fosters trust and facilitates a more efficient and successful legal process.

Potential Outcomes: How To Sue My Car Insurance Company With A Lawyer’s Help

Suing your insurance company can be a complex and stressful process. The outcome is never guaranteed, and the path to resolution can be lengthy and unpredictable. Understanding the potential outcomes, both positive and negative, is crucial before embarking on legal action. This section Artikels the various possibilities, helping you to manage expectations and prepare for different scenarios.The possible outcomes of a lawsuit against an insurance company generally fall into three main categories: settlement, judgment after trial, and appeal.

Each has significant implications for your financial situation and future legal recourse.

Settlement

A settlement occurs when both parties, you and the insurance company, reach an agreement outside of court. This often involves the insurance company offering a sum of money in exchange for you dropping the lawsuit. Settlements can be negotiated at any point during the legal process, even before a trial begins. The amount offered will depend on several factors, including the strength of your case, the evidence you possess, and the insurance company’s assessment of their liability.

For example, a strong case with compelling evidence might lead to a higher settlement offer, while a weaker case might result in a lower offer or even a rejection of your claim. Reaching a settlement can be a faster and less expensive way to resolve the dispute than going to trial.

Judgment After Trial

If a settlement cannot be reached, the case will proceed to trial. The judge or jury will hear evidence from both sides and render a verdict. A judgment in your favor means the court has ruled in your favor, ordering the insurance company to pay you a specific amount of money. Conversely, a judgment against you means the court has dismissed your case, and you may be responsible for paying the insurance company’s legal fees.

The financial implications of a judgment can be significant, whether you win or lose. Winning could provide compensation for damages, lost wages, and legal fees. Losing could leave you responsible for substantial debt and legal costs. For instance, in a case involving a significant injury claim, a favorable judgment might award hundreds of thousands of dollars, whereas an unfavorable outcome could lead to crippling debt.

Appeals

Either party can appeal a court’s decision. An appeal involves asking a higher court to review the lower court’s judgment. Appeals are complex, costly, and time-consuming. They often involve detailed legal arguments and extensive documentation. The higher court might uphold the lower court’s decision, reverse it, or send the case back to the lower court for further proceedings.

The likelihood of success on appeal depends heavily on the specifics of the case and the legal arguments presented. A successful appeal could overturn an unfavorable judgment, while an unsuccessful appeal could solidify an unfavorable ruling, potentially adding further legal costs. For example, an appeal might focus on a point of law that the lower court misinterpreted, arguing that this misinterpretation affected the outcome of the case.

Flowchart of Potential Lawsuit Paths

The following flowchart visually represents the different paths a lawsuit against an insurance company might take:[Imagine a flowchart here. The flowchart would begin with “Filing a Lawsuit.” Branching from this would be “Settlement Negotiations.” If successful, the path ends with “Case Resolved via Settlement.” If unsuccessful, it proceeds to “Trial.” From “Trial,” two branches emerge: “Judgment in Favor of Plaintiff” and “Judgment in Favor of Defendant.” Each of these branches could then lead to “Appeal” with subsequent branches for “Appeal Successful” and “Appeal Unsuccessful.” Each endpoint (Settlement, Judgment for Plaintiff, Judgment for Defendant, Appeal Successful, Appeal Unsuccessful) would have a brief description of the outcome.]